Last month, a transport company owner from Kanpur called us in a panic.

He had just received a notice. Not from a client. From the GST department. His e-way bill had expired mid-route — his driver got stuck at a toll plaza for four hours because of a state highway blockade — and now he was looking at a Rs.10,000 penalty because nobody updated the validity extension in time.

He hadn’t done anything wrong. His consignment was legitimate. His truck was on the road. But the paperwork didn’t keep up with the road, and that gap cost him.

This is not a rare story. It plays out dozens of times a day across India’s transport sector — a sector where 85-90% of fleet operators are small or medium businesses, most running 1 to 20 trucks, and almost none of them with a dedicated compliance team watching the clock.

Here are the five billing mistakes that actually cost small transporters money — not because they’re careless, but because nobody explained the rules clearly.

1. Treating the E-Way Bill Like a One-Time Task

The e-way bill isn’t paperwork you generate before a trip and forget. It’s a live document with a validity clock running from the moment you enter the vehicle number in Part B. The math is straightforward: one day of validity per 200 km for regular cargo. A Delhi-Mumbai run of roughly 1,400 km gives you 7 days — which sounds comfortable until you factor in a breakdown near Surat, a weighbridge queue in Vapi, or a buyer who reschedules unloading by two days.

The rules have tightened. E-way bills can only be generated against documents dated within the last 180 days, which means you can’t backdate old consignments anymore. And since April 2025, multi-factor authentication is mandatory on the GST portal, so your driver or accountant can’t log in from a roadside dhaba on a basic phone as easily as before.

Practical fix

Check e-way bill validity every morning for active consignments. If a trip is getting delayed, extend the validity within the 8-hour window before expiry — the portal allows this with a valid reason. A phone reminder the evening before expiry takes 30 seconds and saves Rs.10,000.

2. Getting the GTA vs. Non-GTA Classification Wrong

Under GST, a Goods Transport Agency is specifically defined as a transporter who issues a consignment note. That’s the defining document. If you’re moving goods and handing over a proper consignment note, you’re a GTA. If you’re an individual truck owner who picks up goods and drops them off without issuing one — you’re not a GTA, and your services are exempt from GST entirely.

This matters for billing because the moment you issue a consignment note to a registered business client, the Reverse Charge Mechanism kicks in — meaning your client is supposed to pay the GST on your freight, not you. At 5%, on freight. The confusion happens in two directions: small transporters who are issuing consignment notes don’t realise they’ve made themselves a GTA and start raising invoices with the wrong GST treatment. And clients who should be paying RCM don’t, assuming the transporter will handle it.

The result: a mismatch in GSTR filings, mismatched ITC claims, and eventually a notice. As of the 56th GST Council Meeting, GTAs now have two choices — 5% without ITC under RCM, or 18% with ITC under forward charge (Annexure V filing required at the start of the financial year). If you haven’t filed Annexure V, you’re in the RCM bucket by default. Know which one you’re in — and make sure your invoice says so clearly. In Transport Logistic, the GST Mode field on every invoice is set explicitly: RCM or forward charge. There’s no ambiguity for either party.

Transport Logistic by SoftwareWale handles GST mode selection, consignment notes, and e-way bill tracking in one place. See how it works.

Talk to Us on WhatsApp →3. Splitting Loading, Unloading, and Storage Into Separate Invoices

Your client asks you to handle loading at the origin, unloading at the destination, and three days of temporary storage. You raise three separate invoices because “different services, different charges.” Reasonable logic — but wrong under GST.

As clarified in the 54th GST Council Meeting (September 2024), when a GTA provides ancillary services like loading, unloading, packing, and temporary warehousing as part of the same consignment — covered by the same consignment note — everything is taxed at the same rate as the primary transport service. This is a composite supply. Splitting it into separate invoices doesn’t just create paperwork confusion; it creates a compliance problem. One well-structured invoice covering freight, loading, and storage is both cleaner and more legally correct.

4. Missing the 30-Day E-Invoice Upload Window

If your annual turnover crosses Rs.10 crore, e-invoicing is mandatory. And since April 2025, the IRP rejects any invoice older than 30 days. This catches transport companies during busy seasons — October trips piling up, invoices uploaded in December. The portal won’t accept them. No IRN. Technically invalid.

The fix is a workflow discipline, not a software purchase: invoices get uploaded within 48 hours of issue. Month-end batching is the enemy of e-invoicing compliance.

5. Not Keeping a Consignment Register

This one isn’t about GST penalties. It’s about business survival.

Most small transporters in India raise invoices in a notebook, WhatsApp messages, or Excel sheets on one person’s laptop. When a dispute comes — and disputes come, over freight amounts, payment dates, loading damage — there’s no clean record to go back to. A proper consignment register tracks vehicle number, driver name, origin, destination, client name, freight amount, GST treatment, e-way bill number, delivery confirmation, and payment status.

If you’re doing this manually: a spreadsheet with these columns takes 15 minutes to build and saves hours in disputes and days during audits. If you want it built into your billing system, the Transport Logistic platform maintains a live invoice register with payment status — Paid, Unpaid, or Partially Paid — for every consignment.

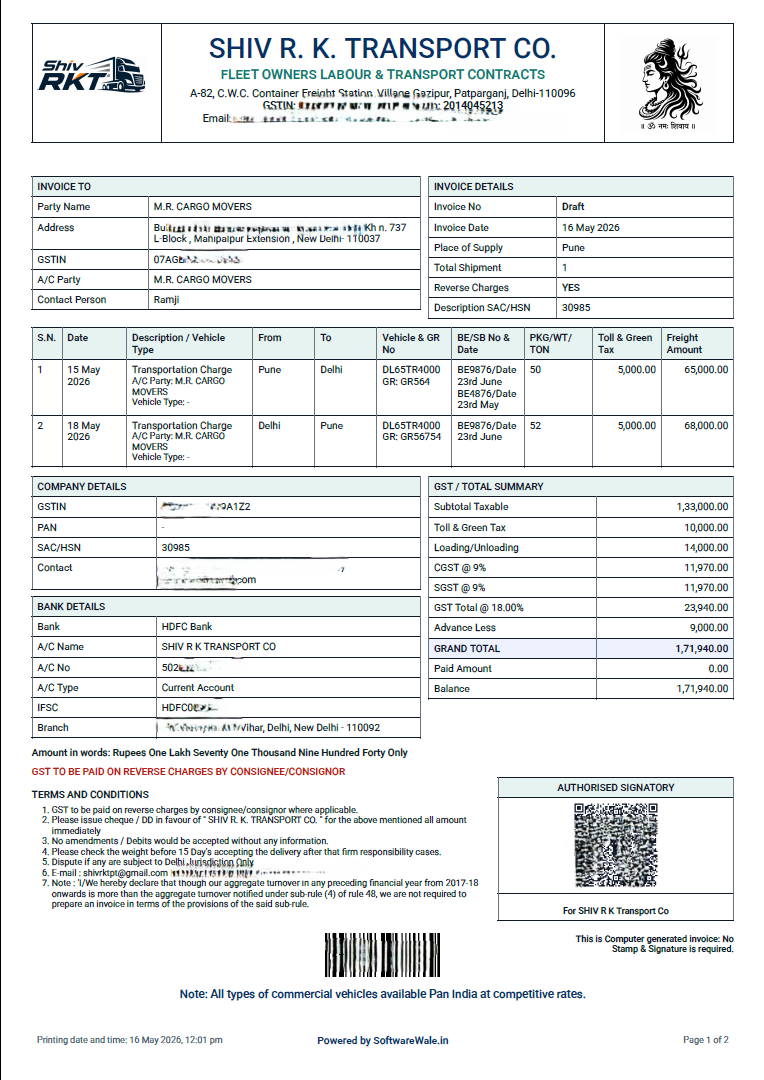

A Transport Logistic invoice PDF — GST mode, consignment details, and bank info all in one clean document.

The Bigger Picture

India’s road transport market is heading toward Rs.192 billion by 2028. The compliance burden has gone up — MFA, 30-day e-invoice windows, 180-day e-way bill rules — while the tools available to small transporters haven’t always kept up. The transport operators who thrive in this environment are the ones who stop treating billing as a formality and start treating it as the backbone of their operations.

None of the five mistakes above requires a major overhaul to fix. Most of them require a habit change, a checklist, and clarity on which category you fall into. Start there.